Why Owning a Home Is a Powerful Financial Decision

In today’s housing market, there are clear financial benefits to owning a home: increasing equity, the chance to build your net worth, and appreciating home values, just to name a few. If you’re a renter, it’s never too early to think about how homeownership can propel you toward a stronger future. Here’s a dive into three often-overlooked financial benefits of homeownership and how preparing for them now can steer you in the direction of greater financial security and savings.

1. You Won’t Always Have a Monthly Housing Payment

Personal finance advisor Dave Ramsey explains:

“Every payment brings you closer to owning the house. When you pay your rent, that money is spent. Gone. Bye. Not returning. But when you pay your mortgage, you work toward full ownership.”

As a homeowner, you can eventually eliminate the monthly payment you make on your house. That’s a huge win and a big factor in how homeownership can drive stability and savings in your life. As soon as you buy a home, your monthly housing costs begin to work for you as forced savings in the form of equity. When you build equity and grow your net worth, you can continue to reinvest those savings into your future, maybe even by buying that next dream home. The possibilities are truly endless.

2. Homeownership Is a Tax Break

One thing people who have never owned a home don’t always think about are the tax advantages of homeownership. The same article states:

“You have tax advantages. Many of the costs of owning a home—like property taxes—are tax deductible. And if you’re paying off a mortgage, you’ll get to count your mortgage interest as a deduction when you file your tax return.”

Whether you’re living in your first home or your fifth, it’s a huge financial advantage to have some tax relief tied to the interest you pay each year. It’s one thing you definitely don’t get when you’re renting. Be sure to work with a tax professional to get the best possible benefits on your annual return.

3. Monthly Housing Costs Are Predictable

A third benefit is the fact that monthly costs start to become more predictable with homeownership, something that doesn’t happen if you’re renting. Ramsey also notes:

“Rent rates will go up. Even if you found a killer deal in a hot area, inflation, competition, and rising property values will cause your rent to go up year after year.”

With a mortgage, you can keep your monthly housing costs relatively steady and predictable. Your monthly costs are most likely based on a fixed-rate mortgage, which allows you to budget your finances over a longer period of time. Rental prices have been since skyrocketing 2012, and with today’s low mortgage rates, it’s a great time to get more for your money when purchasing a home. If you want to lock-in your monthly payment at a low rate and have a solid understanding of what you’re going to spend in your mortgage payment each month, buying a home may be your best bet.

Bottom Line

If you’re ready to start feeling the benefits of stability, savings, and predictability that come with owning a home, let’s connect to determine if buying sooner rather than later is right for you.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

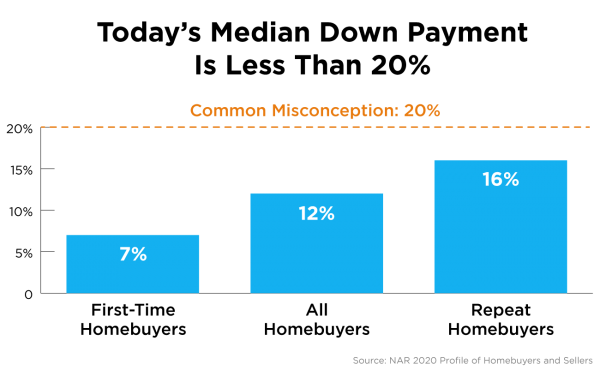

Do I Really Need a 20% Down Payment to Buy a Home?

Is the idea of saving for a down payment holding you back from buying a home right now? You may be eager to take advantage of today’s low mortgage rates, but the thought of needing a large down payment might make you want to pump the brakes. Today, there’s still a common myth that you have to come up with 20% of the total sale price for your down payment. This means people who could buy a home may be putting their plans on hold because they don’t have that much saved yet. The reality is, whether you’re looking for your first home or you’ve purchased one before, you most likely don’t need to put 20% down. Here’s why.

According to Freddie Mac:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

If saving that much money sounds daunting, potential homebuyers might give up on the dream of homeownership before they even begin – but they don’t have to.

Data in the 2020 Profile of Home Buyers and Sellers from the National Association of Realtors (NAR) indicates that the median down payment actually hasn’t been over 20% since 2005, and even then, that was for repeat buyers, not first-time homebuyers. As the image below shows, today’s median down payment is clearly less than 20%.

What does this mean for potential homebuyers?

As we can see, the median down payment was lowest for first-time buyers with the 2020 percentage coming in at 7%. If you’re a first-time buyer and putting down 7% still seems high, understand that there are programs that allow qualified buyers to purchase a home with a down payment as low as 3.5%. There are even options like VA loans and USDA loans with no down payment requirements for qualified applicants.

It’s important for potential homebuyers (whether they’re repeat or first-time buyers) to know they likely don’t need to put down 20% of the purchase price, but they do need to do their homework to understand the options available. Be sure to work with trusted professionals from the start to learn what you may qualify for in the homebuying process.

Bottom Line

Don’t let down payment myths keep you from hitting your homeownership goals. If you’re hoping to buy a home this year, let’s connect to review your options.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Want to Build Wealth? Buy a Home This Year.

Every year, households across the country make the decision to rent for another year or take the leap into homeownership. They look at their earnings and savings and then decide what makes the most financial sense. That equation will most likely take into consideration monthly housing costs, tax advantages, and other incremental expenses. Using these measurements, recent studies show that it’s still more affordable to own than rent in most of the country.

There is, however, another financial advantage to owning a home that’s often forgotten in the analysis – the wealth built through equity when you own a home.

Odeta Kushi, Deputy Chief Economist for First American, discusses this point in a recent blog post. She explains:

“Once you include the equity benefit of price appreciation, owning made more financial sense than renting in 48 out of the 50 top markets, with the only exceptions being San Francisco and San Jose, Calif.”

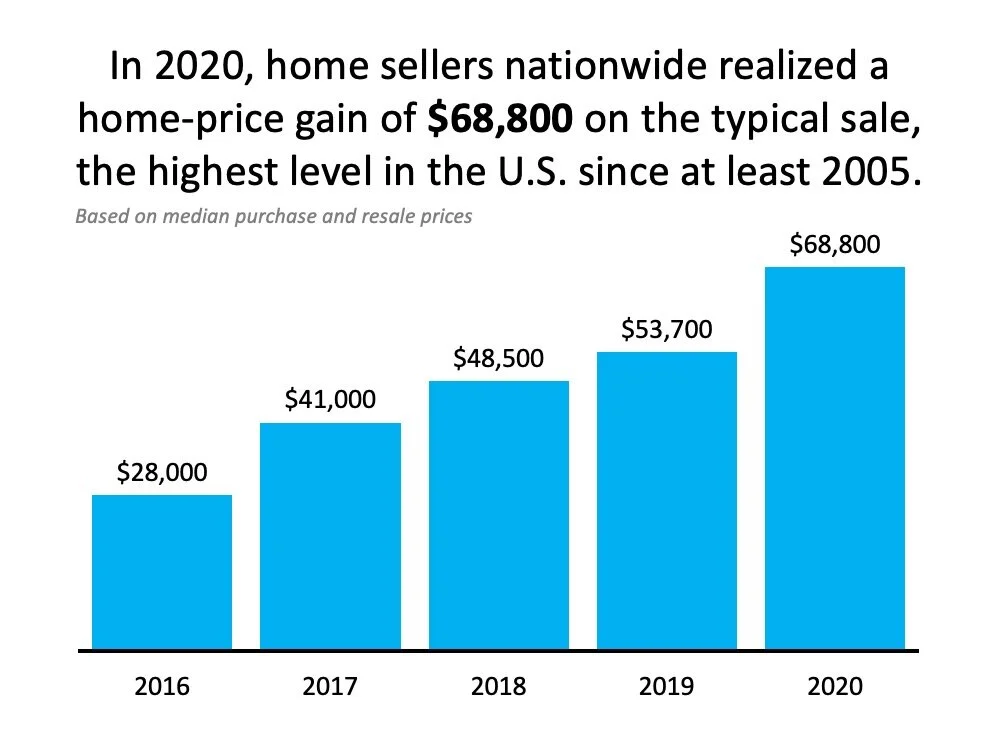

What has this equity piece meant to homeowners in the past?

ATTOM Data Solutions, the curator of one of the nation’s premier property databases, just analyzed the typical home-price gain owners nationwide enjoyed when they sold their homes. Here’s a breakdown of their findings:

The typical gain in the sale of the home (equity) has increased significantly over the last five years.

CoreLogic, another property data curator, also weighed in on the subject. According to their latest Homeowner Equity Insights Report, the average homeowner gained $17,000 in equity in just the last year alone.

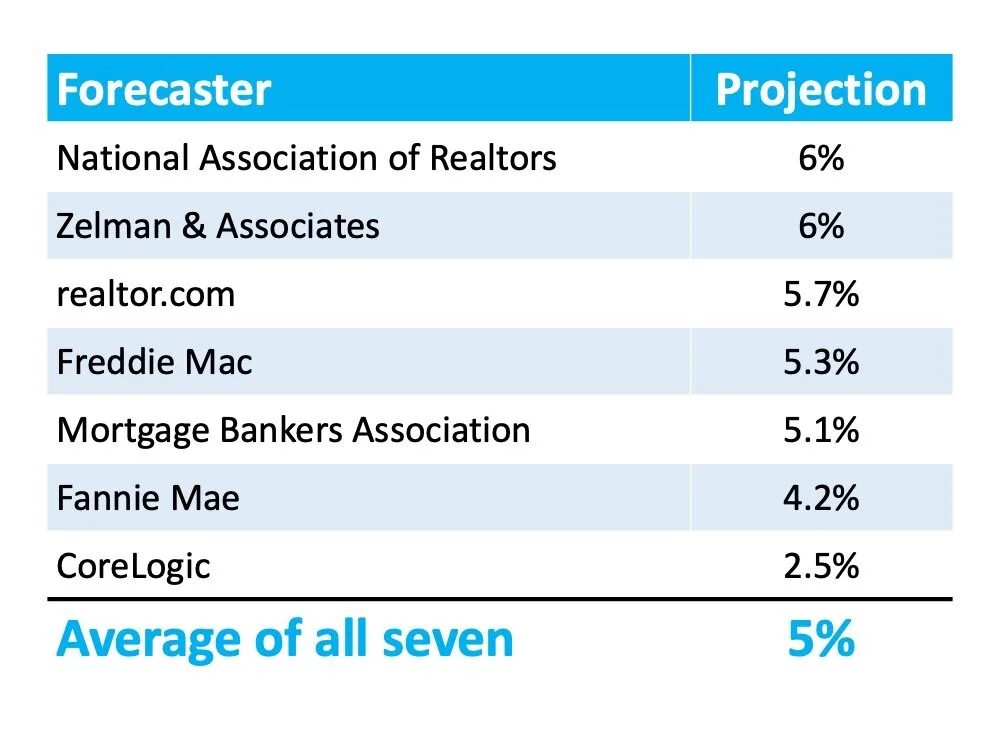

What does the future look like for homeowners when it comes to equity?

Here are the seven major home price appreciation forecasts for 2021:

The National Association of Realtors (NAR) just reported that today, the median-priced home in the country sells for $309,800. If homes appreciate by 5% this year (the average of the forecasts), the homeowner will increase their wealth by $15,490 in 2021 through increased equity.

Bottom Line

As you make your plans for the coming year, be sure to consider the equity benefits of home price appreciation as you weigh the financial advantages of buying over renting. When you do, you may find this is the perfect time to jump into homeownership.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Turn to an Expert for the Best Advice, Not Perfect Advice

As we approach the anniversary of the hardships we’ve faced through this pandemic and the subsequent recession, it’s normal to reflect on everything that’s changed and wonder what’s ahead for 2021. While there are signs of economic recovery as vaccines are being issued, we still have a long way to go. It’s at times like these we want exact information about anything we’re doing. That information brings knowledge, and this gives us a sense of relief and comfort in uncertain times.

If you’re thinking about buying or selling a home today, the same need for information is very real. But, because it’s such a big step in our lives, that desire for clear information is even greater in the homebuying or selling process. Given the current level of overall anxiety, we want that advice to be truly perfect. The challenge is, no one can give you “perfect” advice. Experts can, however, give you the best advice possible.

Let’s say you need an attorney, so you seek out an expert in the type of law required for your case. When you go to her office, she won’t immediately tell you how the case is going to end or how the judge or jury will rule. If she could, that would be perfect advice. What a good attorney can do, however, is discuss with you the most effective strategies you can take. She may recommend one or two approaches she believes will be best for your case.

She’ll then leave you to make the decision on which option you want to pursue. Once you decide, she can help you put a plan together based on the facts at hand. She’ll help you achieve the best possible resolution and make whatever modifications in the strategy are necessary to guarantee that outcome. That’s an example of the best advice possible.

The role of a real estate professional is just like the role of a lawyer. An agent can’t give you perfect advice because it’s impossible to know exactly what’s going to happen throughout the transaction – especially in this market.

An agent can, however, give you the best advice possible based on the information and situation at hand, guiding you through the process to help you make the necessary adjustments and best decisions along the way. An agent will lead you to the best offer available. That’s exactly what you want and deserve.

Bottom Line

If you’re thinking of buying or selling this year, let’s connect to make sure you get the best advice possible.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

What Record-Low Housing Inventory Means for You

The real estate market is expected to do very well in 2021, with mortgage rates that are hovering at historic lows and forecasted by experts to remain favorable throughout the year. One challenge to the housing industry, however, is the lack of homes available for sale today. Last week, the National Association of Realtors (NAR) released their Existing Home Sales Report, which shows that the inventory of homes for sale is currently at an all-time low. The report explains:

“Total housing inventory at the end of December totaled 1.07 million units, down 16.4% from November and down 23% from one year ago (1.39 million). Unsold inventory sits at an all-time low 1.9-month supply at the current sales pace, down from 2.3 months in November and down from the 3.0-month figure recorded in December 2019. NAR first began tracking the single-family home supply in 1982.”

(See graph below):

What Does This Mean for You?

If You’re a Buyer:

Be patient during your home search. It may take time to find a home you love. Once you do, however, be ready to move forward quickly. Get pre-approved for a mortgage, be prepared to make a competitive offer from the start, and know that a shortage in inventory could mean you’ll enter a bidding war. Calculate just how far you’re willing to go to secure a home and lean on your real estate professional as an expert guide along the way. The good news is, more inventory is likely headed to the market soon, Lawrence Yun, Chief Economist at NAR, notes:

“To their credit, homebuilders and construction companies have increased efforts to build, with housing starts hitting an annual rate of near 1.7 million in December, with more focus on single-family homes…However, it will take vigorous new home construction in 2021 and in 2022 to adequately furnish the market to properly meet the demand.”

If You’re a Seller:

Realize that, in some ways, you’re in the driver’s seat. When there’s a shortage of an item at the same time there’s a strong demand for it, the seller is in a good position to negotiate the best possible terms. Whether it’s the price, moving date, possible repairs, or anything else, you’ll be able to request more from a potential purchaser at a time like this – especially if you have multiple interested buyers. Don’t be unreasonable, but understand you probably have the upper hand.

Bottom Line

The housing market will remain strong throughout 2021. Know what that means for you, whether you’re buying, selling, or doing both.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

What Happens When Homeowners Leave Their Forbearance Plans?

According to the latest report from Black Knight, Inc., a well-respected provider of data and analytics for mortgage companies, 6.48 million households have entered a forbearance plan as a result of financial concerns brought on by the COVID-19 pandemic. Here’s where these homeowners stand right now:

2,543,000 (39%) are current on their payments and have left the program

625,000 (9%) have paid off their mortgages

434,000 (7%) have negotiated a repayment plan and have left the program

2,254,000 (35%) have extended their original forbearance plan

512,000 (8%) are still in their original forbearance plan

116,000 (2%) have left the program and are still behind on payments

This shows that of the almost 3.72 million homeowners who have left the program, only 116,000 (2%) exited while they were still behind on their payments. There are still 2.77 million borrowers in a forbearance program. No one knows for sure how many of those will become foreclosures. There are, however, three major reasons why most experts believe there will not be a tsunami of foreclosures as we saw during the housing crash over a decade ago:

Almost 30% of borrowers in forbearance are still current on their mortgage payments.

Banks likely don’t want to repeat the mistakes of 2008-2012 when they put large numbers of foreclosures on their books. This time, many will instead negotiate a modification plan with the borrower, which will enable households to maintain ownership of the home.

With the significant equity homeowners have today, many will be able to sell instead of going into foreclosure.

Will there be foreclosures coming to the market? Yes. There are hundreds of thousands of foreclosures in this country each year. People experience economic hardships, and in some cases, are not able to meet their mortgage obligations.

Here’s the breakdown of new foreclosures over the last three years, prior to the pandemic:

2017: 314,220

2018: 279,040

2019: 277,520

Through the first three quarters of 2020 (the latest data available), there were only 114,780 new foreclosures. If 10% of those currently in forbearance go to foreclosure, 275,000 foreclosures would be added to the market in 2021. That would be an average year as the numbers above show.

What happens if the number is more than 10%?

If we do experience a higher foreclosure rate from those in forbearance, most experts believe the current housing market will easily absorb the excess inventory. We entered 2020 with 1,210,000 single-family homes available for purchase. At the time, that was low and problematic. The market was experiencing high buyer demand, and we needed more houses to meet that demand. We’re now entering 2021 with 320,000 fewer homes for sale, while buyer demand remains extremely strong. This means the housing market has the capacity to soak up a lot of inventory.

Bottom Line

There will be more foreclosures entering the market later this year, especially compared to the record-low numbers in 2020. However, the market will be able to handle the increase as buyer demand remains strong.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

What’s the Difference between an Appraisal and a Home Inspection?

If you’re planning to buy a home, an appraisal is an important step in the process. It’s a professional evaluation of the market value of the home you’d like to buy. In most cases, an appraisal is ordered by the lender to confirm or verify the value of the home prior to lending a buyer money for the purchase. It’s also a different step in the process from a home inspection, which assesses the condition of the home before you finalize the transaction. Here’s the breakdown of each one and why they’re both important when buying a home.

Home Appraisal

The National Association of Realtors (NAR) explains:

“A home purchase is typically the largest investment someone will make. Protect yourself by getting your investment appraised! An appraiser will observe the property, analyze the data, and report their findings to their client. For the typical home purchase transaction, the lender usually orders the appraisal to assist in the lender’s decision to provide funds for a mortgage.”

When you apply for a mortgage, an unbiased appraisal (which is required by the lender) is the best way to confirm the value of the home based on the sale price. Regardless of what you’re willing to pay for a house, if you’ll be using a mortgage to fund your purchase, the appraisal will help make sure the bank doesn’t loan you more than what the home is worth.

This is especially critical in today’s sellers’ market where low inventory is driving an increase in bidding wars, which can push home prices upward. When sellers are in a strong position like this, they tend to believe they can set whatever price they want for their house under the assumption that competing buyers will be willing to pay more.

However, the lender will only allow the buyer to borrow based on the value of the home. This is what helps keep home prices in check. If there’s ever any confusion or discrepancy between the appraisal and the sale price, your trusted real estate professional will help you navigate any additional negotiations in the buying process.

Home Inspection

Here’s the key difference between an appraisal and an inspection. MSN explains:

“In simplest terms, a home appraisal determines the value of a home, while a home inspection determines the condition of a home.”

The home inspection is a way to determine the current state, safety, and condition of the home before you finalize the sale. If anything is questionable in the inspection process – like the age of the roof, the state of the HVAC system, or just about anything else – you as a buyer have the option to discuss and negotiate any potential issues or repairs with the seller before the transaction is final. Your real estate agent is a key expert to help you through this part of the process.

Bottom Line

The appraisal and the inspection are critical steps when buying a home, and you don’t need to manage them by yourself. Let’s connect today so you have the expert guidance you need to navigate through the entire homebuying process.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Why Moving May Be Just the Boost You Need

As we look back over the past year, we’ve certainly lived through one of the most stressful periods in recent history. After spending so much more time at home throughout the health crisis, some are wondering if they should move to improve their mental health and well-being. This is no surprise since the U.S. Census Bureau reported an increase in the percentage of adults with symptoms of anxiety and depression in a recent Household Pulse Survey.

There’s logic behind the idea that making a move could improve someone’s quality of life. When people change their scenery, they often feel happier. Catherine Hartley, an Assistant Professor at New York University’s Department of Psychology and co-author of a study on how new experiences impact happiness, mentioned:

“Our results suggest that people feel happier when they have more variety in their daily routines—when they go to novel places and have a wider array of experiences.”

If you’re looking for a new experience, planning a move into a new home may be something you’ve started to consider more carefully. If so, you’re not alone. The 2020 Annual National Movers Study by United Van Lines shows:

“For customers who cited COVID-19 as an influence on their move in 2020, the top reasons associated with COVID-19 were concerns for personal and family health and wellbeing (60%); desires to be closer to family (59%); 57% moved due to changes in employment status or work arrangement (including the ability to work remotely); and 53% desired a lifestyle change or improvement of quality of life.”

So, if you’re thinking of moving this year to help boost your happiness factor, here are a few questions to ask yourself as you make your decision.

How’s the Weather?

Is the weather something that’s important to you? Does it have a tendency to impact your mood? The World Population Review shares:

“What states have the best weather? When evaluating each state for temperature, rain, and sun, some states stand out. Although climate and weather preferences are personal and subjective, some criteria are considered to make up the best weather, according to Current Results:

Comfortable temperatures from 63°F to 86°F for more than half of the year.Dry weather with no more than 60 inches of rain per year.Mostly clear skies with an average of sunshine for at least 60% of the year.”

“Better weather” can mean different things to different people – some prefer the heat, others cooler temperatures, and some want to experience all four seasons. Think about what makes you feel happiest if you’re looking for a new location.

Should I Choose the City, Suburbs, or Country?

With the COVID-19 pandemic, some people are deciding to move to lower-density areas. Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), mentions:

“The third quarter Home Building Geography Index (HBGI) reveals that a suburban shift for consumer home buying preferences in the wake of the COVID-19 pandemic is accelerating as telecommuting is providing consumers more flexibility to live further out within large metros or even to relocate to more affordable, smaller metro areas.”

Can you work from home? Are you open to a longer commute in the future? If so, a move to the suburbs or even a quieter rural area may be a win for you. Or, if you’ve always dreamed of life in the city, now may be your chance to move into town.

Bottom Line

As we look beyond the trials of the pandemic, many are hoping for a new beginning, and that may mean moving. Let’s connect today to talk about your new goals and options in today’s market.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

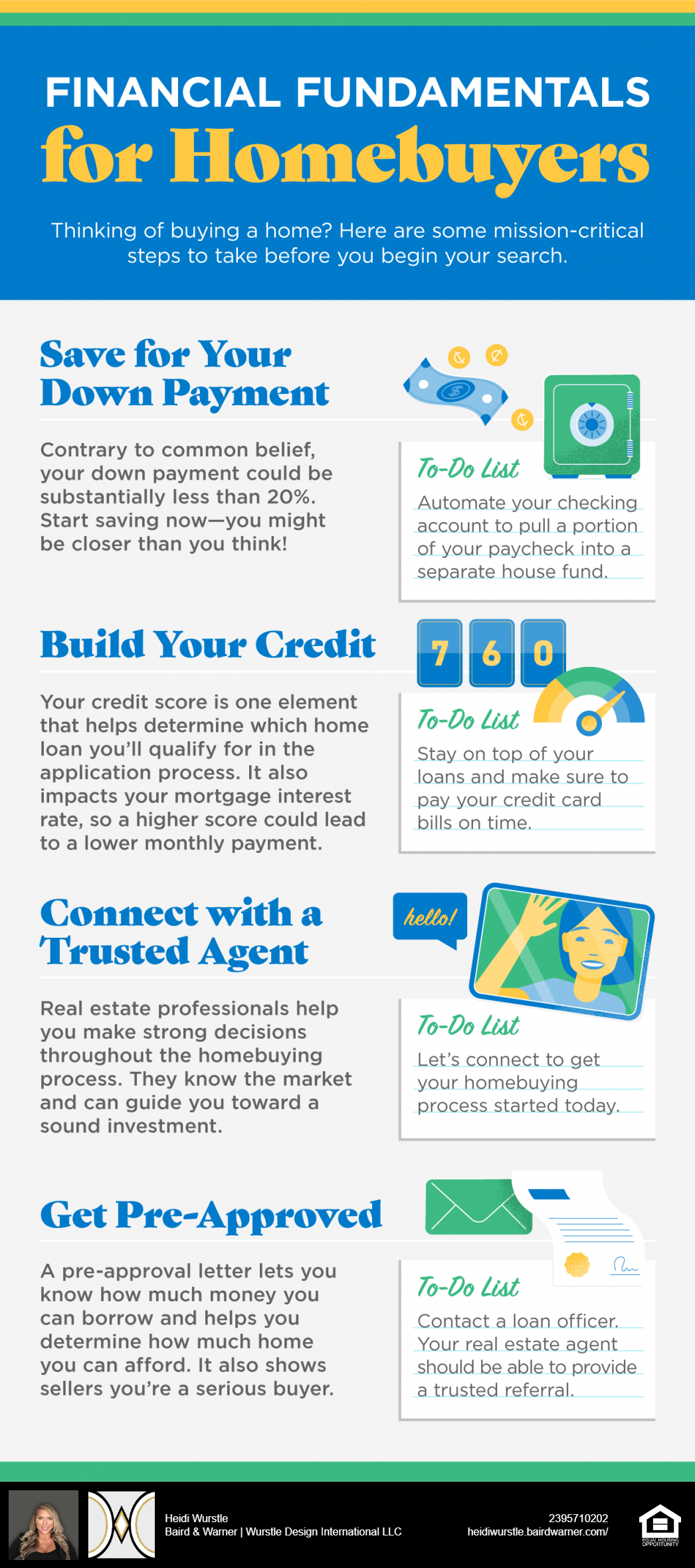

Financial Fundamentals for Homebuyers

Some Highlights

When you’re thinking about buying a home, there are a few key steps to take before you even start to look at houses.

From saving for your down payment to getting pre-approved for a mortgage, you’ll want to make sure you keep your financial plan on track from the beginning.

Let’s connect today to make sure you have an introduction to a trusted lender and the best possible real estate guidance as you begin your homebuying process.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

What Experts Are Saying about the 2021 Job Market

Earlier this month, the Bureau of Labor Statistics (BLS) released their most recent Jobs Report. The report revealed that the economy lost 140,000 jobs in December. That’s a devastating number and dramatically impacts those households that lost a source of income. However, we need to give it some context. Greg Ip, Chief Economics Commentator at the Wall Street Journal (WSJ), explains:

“The economy is probably not slipping back into recession. The drop was induced by new restrictions on activity as the pandemic raged out of control. Leisure and hospitality, which includes restaurants, hotels, and amusement parks, tumbled 498,000.”

In the same report, Michael Pearce, Senior U.S. Economist of Capital Economics, agreed:

“The 140,000 drop in non-farm payrolls was entirely due to a massive plunge in leisure and hospitality employment, as bars and restaurants across the country have been forced to close in response to the surge in coronavirus infections. With employment in most other sectors rising strongly, the economy appears to be carrying more momentum into 2021 than we had thought.”

Once the vaccine is distributed throughout the country and the pandemic is successfully under control, the vast majority of those 480,000 jobs will come back.

Here are two additional comments from other experts, also reported by the WSJ that day:

Nick Bunker, Head of Research in North America for Indeed:

“These numbers are distressing, but they are reflective of the time when coronavirus vaccines were not rolled out and federal fiscal policy was still deadlocked. Hopefully, the recent legislation can help build a bridge to a time when vaccines are fully rolled out and the labor market can sustainably heal.”

Michael Feroli, Chief U.S. Economist for JPMorgan Chase:

“The good news in today’s report is that outside the hopefully temporary hit to the food service industry, the rest of the labor market appears to be holding in despite the latest public health challenges.”

What impact will this have on the real estate market in 2021?

Some are concerned that with millions of Americans unemployed, we may see distressed properties (foreclosures and short sales) dominate the housing market once again. Rick Sharga, Executive Vice President at RealtyTrac, along with most other experts, doesn’t believe that will be the case:

“There are reasons to be cautiously optimistic despite massive unemployment levels and uncertainty about government policies under the new Administration. But while anything is possible, it’s highly unlikely that we’ll see another foreclosure tsunami or housing market crash.”

Bottom Line

For the households that lost a wage earner, these are extremely difficult times. Hopefully, the new stimulus package will lessen some of their pain. The health crisis, however, should vastly improve by mid-year with expectations that the jobs market will also progress significantly.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Owning a Home Is Still More Affordable Than Renting One

If spending more time at home over the past year is making you really think hard about buying a home instead of renting one, you’re not alone. You may be wondering, however, if the dollars and cents add up in your favor as home prices continue to rise. According to the experts, in many cases, it’s still more affordable to buy a home than rent one. Here’s why.

ATTOM Data Solutions recently released the 2021 Rental Affordability Report, which states:

“Owning a median-priced three-bedroom home is more affordable than renting a three-bedroom property in 572, or 63 percent of the 915 U.S. counties analyzed for the report.

That has happened even though median home prices have increased more than average rents over the past year in 83 percent of those counties and have risen more than wages in almost two-thirds of the nation.”

How is this possible?

The answer: historically low mortgage interest rates. Todd Teta, Chief Product Officer with ATTOM Data Solutions, explains:

“Home-prices are rising faster than rents and wages in a majority of the country. Yet, home ownership is still more affordable, as amazingly low mortgage rates that dropped below 3 percent are helping to keep the cost of rising home prices in check.”

In 2020, mortgage rates reached all-time lows 16 times, and so far, they’re continuing to hover in low territory this year. These low rates are a big factor in driving affordability. Teta also notes:

“It’s startling to see that kind of trend. But it shows how both the cost of renting has been relatively high compared to the cost of ownership and how declining interest rates are having a notable impact on the housing market and home ownership. The coming year is totally uncertain, amid so many questions connected to the Coronavirus pandemic and the broader economy. But right now, owning a home still appears to be a financially-sound choice for those who can afford it.”

Bottom Line

If you’re considering buying a home this year, let’s connect today to discuss the options that match your budget while affordability is in your favor.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Should I Wait for Lower Mortgage Interest Rates?

Historically low mortgage rates are a big motivator for homebuyers right now. In 2020 alone, rates hit new record-lows 16 times, and the trend continued into the early part of this year. Many hopeful homebuyers are now wondering if they should put their plans on hold and wait for the lowest rates imaginable. However, the reality is, acting sooner rather than later may be the actual win if you’re ready to buy a home.

According to Greg McBride, Chief Financial Analyst for Bankrate:

“As vaccines become more widely available and a return to normal starts to come into view, we’ll see mortgage rates bounce off the record lows.”

While only a slight increase in mortgage rates is projected for 2021, some experts believe they will start to rise. Over the past week, for example, the average mortgage rate ticked up slightly, reaching 2.79%. This is still incredibly low compared to the trends we’ve seen over time. According to Freddie Mac:

“Borrowers are smart to take advantage of these low rates now and will certainly benefit as a result.”

Here’s why.

As mortgage rates rise, the increase impacts the overall cost of purchasing a home. The higher the rate, the higher your monthly mortgage payment, especially as home prices rise too. Sam Khater, Chief Economist at Freddie Mac, says:

“The forces behind the drop in rates have been shifting over the last few months and rates are poised to rise modestly this year. The combination of rising mortgage rates and increasing home prices will accelerate the decline in affordability and further squeeze potential homebuyers during the spring home sales season.”

What does this mean for buyers?

Right now, the inventory of houses for sale is also at a historic low, making it more challenging than normal to find a home to buy in many areas. As more buyers hit the market in the typically busy spring buying season, it may become even harder to find a home in the coming months. With this in mind, Len Keifer, Deputy Chief Economist for Freddie Mac, recommends taking advantage of both low mortgage rates and the opportunity to buy:

“If you’ve found a home that fits your needs at a price you can afford, it might be better to act now rather than wait for future rate declines that may never come and a future that likely holds very tight inventory.”

Bottom Line

While today’s low mortgage rates provide great opportunities for homebuyers, we may not see them stick around forever. If you’re ready to buy a home, let’s connect so you can take advantage of what today’s market has to offer.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

How to Make the Dream of Homeownership a Reality This Year

In 1963, Martin Luther King, Jr. inspired a powerful movement with his famous “I Have a Dream” speech. Through his passion and determination, he sparked interest, ambition, and courage in his audience. Today, reflecting on his message encourages many of us to think about our own dreams, goals, beliefs, and aspirations. For many Americans, one of those common goals is owning a home: a piece of land, a roof over our heads, and a place where we can grow and flourish.

If you’re dreaming of buying a home this year, start by connecting with a local real estate professional to understand what goes into the process. With a trusted advisor at your side, you can then begin to answer the questions below to set yourself up for homebuying success.

1. How Can I Better Understand the Process, and How Much Can I Afford?

The process of buying a home is not one to enter into lightly. You need to decide on key things like how long you plan on living in an area, school districts you prefer, what kind of commute works for you, and how much you can afford to spend.

Keep in mind, before you start the process to purchase a home, you’ll also need to apply for a mortgage. Lenders will evaluate several factors connected to your financial track record, one of which is your credit history. They’ll want to see how well you’ve been able to minimize past debts, so make sure you’ve been paying your student loans, credit cards, and car loans on time. If your financial situation has changed recently, be sure to discuss that with your lender as well. Most agents have loan officers they trust and will provide referrals for you.

According to ConsumerReports.org:

“Financial planners recommend limiting the amount you spend on housing to 25 percent of your monthly budget.”

2. How Much Do I Need for a Down Payment?

In addition to knowing how much you can afford on a monthly mortgage payment, understanding how much you’ll need for a down payment is another critical step. Thankfully, there are many different options and resources in the market to potentially reduce the amount you may think you need to put down.

If you’re concerned about saving for a down payment, start small and be consistent. A little bit each month goes a long way. Jumpstart your savings by automatically adding a portion of your monthly paycheck into a separate savings account or house fund. AmericaSaves.org says:

“Over time, these automatic deposits add up. For example, $50 a month accumulates to $600 a year and $3,000 after five years, plus interest that has compounded.”

Before you know it, you’ll have enough for a down payment if you’re disciplined and thoughtful about your process.

3. Saving Takes Time: Practice Living on a Budget

As tempting as it is to pass the extra time you may be spending at home these days with a little retail therapy, putting that extra money toward your down payment will help accelerate your path to homeownership. It’s the little things that count, so start trying to live on a slightly tighter budget if you aren’t doing so already. A budget will allow you to save more for your down payment and help you pay down other debts to improve your credit score.

A survey of millennial spending shows, “68% reported that shelter in place orders helped them save for their down payment.” Danielle Hale, Chief Economist at realtor.com, also notes:

“If there is any silver lining to the current economic landscape, it’s that mortgage rates are hanging around record lows…Additionally, shelter-in-place orders helped many who were fortunate enough to keep their jobs save for a down payment — one of the largest hurdles of buying a home. The combination of low rates and the opportunity to save is enabling many millennials to move up their home buying timeline.”

While you don’t need to cut all of the extras out of your current lifestyle, making smarter choices and limiting your spending in areas where you can slim down will make a big difference.

Bottom Line

If homeownership is on your dream list this year, take a good look at what you can prioritize to help you get there. To determine the steps you should take to start the process, let’s connect today.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Things to Avoid after Applying for a Mortgage

Some Highlights

There are a few key things to make sure you avoid after applying for a mortgage to help make sure you still qualify for your loan at the closing table.

Along the way, be sure to discuss any changes in income, assets, or credit with your lender, so you don’t unintentionally jeopardize your application.

The best plan is to fully disclose your intentions with your lender before you do anything financial in nature.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

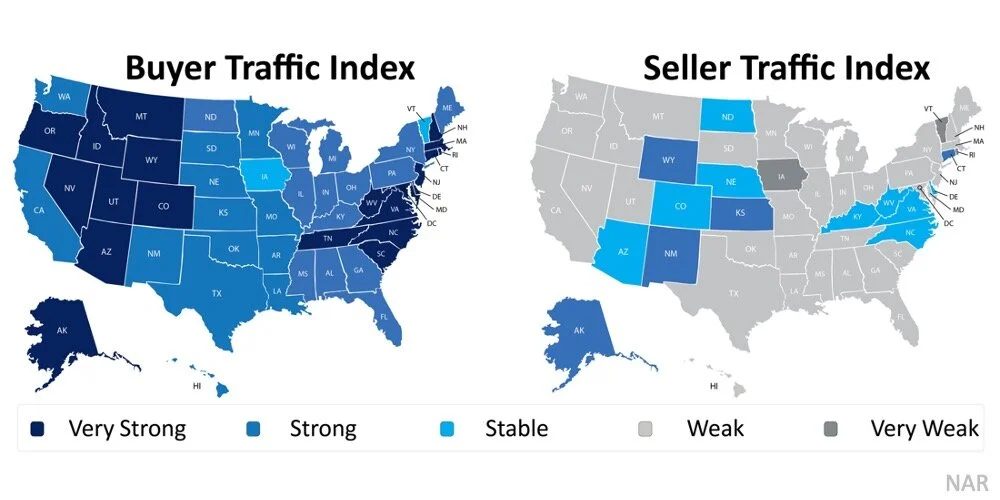

Why Right Now May Be the Time to Sell Your House

The housing market made an incredible recovery in 2020 and is now positioned for an even stronger year in 2021. Record-low mortgage interest rates are a driving factor in this continued momentum, with average rates hovering at historic all-time lows.

According to the latest Realtors Confidence Index Survey from the National Association of Realtors (NAR), buyer demand across the country is incredibly strong. That’s not the case, however, on the supply side. Seller traffic is simply not keeping up. Here’s a breakdown by state:

As the maps show, buyer traffic is high, but seller traffic is low. With so few homes for sale right now, record-low inventory is creating a mismatch between supply and demand.

NAR also just reported that the actual number of homes currently for sale stands at 1.28 million, down 22% from one year ago (1.64 million). Additionally, inventory is at an all-time low with 2.3 months supply available at the current sales pace. In a normal market, that number would be 6.0 months of inventory – significantly higher than it is today.

What does this mean for buyers and sellers?

Buyers need to remain patient in the search process. At the same time, they must be ready to act immediately once they find the right home since bidding wars are more common when so few houses are available for sale.

Sellers may not want to wait until spring to put their houses on the market, though. With such high buyer demand and such a low supply, now is the perfect time to sell a house on optimal terms.

Bottom Line

The real estate market is entering the year like a lion. There’s no indication it will lose that roar, assuming inventory continues to come to market.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Will Forbearance Plans Lead to a Tsunami of Foreclosures?

At the onset of the economic disruptions caused by the COVID pandemic, the government quickly put into place forbearance plans to allow homeowners to remain in their homes without making their monthly mortgage payments. Today, almost three million households are actively in a forbearance plan. Though 29.4% of those in forbearance have continued to stay current on their payments, many have not.

Yanling Mayer, Principal Economist at CoreLogic, recently revealed:

“A distributional analysis of forborne loans’ payment status reveals that more than one third (39.1%) of all forborne loans are now 150+ days behind payment, while as many as 1-in-4 (25.5%) are 180+ days past due.”

These homeowners have been given permission to not make their payments, but the question now is: how many of them will be able to catch up after their forbearance program ends? There’s speculation that a forthcoming wave of foreclosures could be the result, and that could lead to another crash in home values like we saw a decade ago.

However, today’s situation is different than the 2006-2008 housing crisis as many homeowners have tremendous amounts of equity in their homes.

What are the experts saying?

Over the last 30 days, several industry experts have weighed in on this subject.

Michael Sklarz, President at Collateral Analytics:

“We may very well see a meaningful increase in the number of homes listed for sale as these borrowers choose to sell at what is arguably an intermediate top in the market and downsize to more affordable homes rather than face foreclosure.”

Odeta Kushi, Deputy Chief Economist at First American:

“The foreclosure process is based on two steps. First, the homeowner suffers an adverse economic shock…leading to the homeowner becoming delinquent on their mortgage. However, delinquency by itself is not enough to send a mortgage into foreclosure. With enough equity, a homeowner has the option of selling their home, or tapping into their equity through a refinance, to help weather the economic shock. It is a lack of sufficient equity, the second component of the dual trigger, that causes a serious delinquency to become a foreclosure.”

Don Layton, Senior Industry Fellow at the Joint Center for Housing Studies of Harvard University:

“With a greater cushion of equity, troubled homeowners have dramatically improved options: a greater ability to access funding (e.g. home equity lines) to keep paying monthly expenses until family finances might recover, improved ability to qualify for and support a loan modification, and, if push comes to shove, the ability to sell the home and monetize their increased net worth while reducing monthly payment obligations. So, what should lenders and servicers expect: a large number of foreclosures or only a modest increase? I believe the latter.”

With today’s positive equity situation, many homeowners will be able to use a loan modification or refinance to stay in their homes. If not, some will go to foreclosure, but most will be able to sell and walk away with their equity.

Won’t the additional homes on the market impact prices?

Distressed properties (foreclosures and short sales) sell at a significant discount. If homeowners sell instead of going into foreclosure, the impact on the housing market will be much less severe.

We must also realize there is currently an unprecedented lack of inventory on the market. Just last week, realtor.com explained:

“Nationally, the number of homes for sale was down 39.6%, amounting to 449,000 fewer homes for sale than last December.”

It’s important to remember that there weren’t enough homes for sale even then, and inventory has only continued to decline.

The market has the potential to absorb half a million homes this year without it causing home values to depreciate.

Bottom Line

The pandemic has led to both personal and economic hardships for many American households. The overall residential real estate market, however, has weathered the storm and will continue to do so in 2021.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

4 Reasons People Are Buying Homes in 2021

According to many experts, the real estate market is expected to continue growing in 2021, and it’s largely driven by the lasting impact the pandemic is having on our lifestyles. As many of us spend extra time at home, we’re reevaluating what “home” means and what we may need in one going forward.

Here are 4 reasons people are reconsidering where they live and why they’re expecting to buy a home this year.

1. Record-Low Mortgage Interest Rates

In 2020, the average interest rate for a 30-year fixed mortgage hit a record low 16 times, continuing to fall further below 3%. According to Freddie Mac, the average 30-year fixed interest rate today is 2.65%. Many wonder how low these rates will go and how long they’ll last. Len Keifer, Deputy Chief Economist for Freddie Mac, advises:

“If you’ve found a home that fits your needs at a price you can afford, it might be better to act now rather than wait for future rate declines that may never come and a future that likely holds very tight inventory.”

This sense of urgency is driving many to buy this year.

2. Working from Home

Remote work is a new normal for many businesses, and it’s lasting longer than most expected. Many in the workforce today are discovering they don’t need to live close to the office anymore and they can get more for their money by moving a little further outside of the city limits. David Mele, President at Homes.com, says:

“The surge in the work-from-home population has rewritten the playbook for many homebuying and rental decisions, from when and where to relocate, to what people are looking for in their next residence.”

The reality is, for some people, working remotely in their current home is challenging, especially when there may be other options available.

3. More Outdoor Space

Another new priority for homeowners is having more usable outdoor space. Being at home is driving those in some areas to seek less densely populated neighborhoods so they have more room to stretch their legs. In addition, those living in apartments and townhomes are often looking for extra square footage, both inside and out.

According to the State of Home Spending report by HomeAdvisor, of the households surveyed, almost half reported spending 27% more on outdoor living over the past year. This is a trend that’s expected to grow in 2021 and beyond.

4. Avoiding Renovations

It’s recently come to light that many homeowners would also rather buy a new home than go through the process of fixing up the one they have. According to the 2020 Profile of Home Buyers and Sellers report from the National Association of Realtors (NAR), 44% of homebuyers purchased a new home to “avoid renovations or problems with the plumbing or electricity.”

Depending on what needs to be addressed, today’s high buyer demand may make it possible to skip some renovations before selling. Many of these homeowners have prioritized buying over renovating for convenience and potential cost savings.

Bottom Line

It’s clear that homeownership needs are changing. As a result, Americans are expected to move in record numbers this year. If you’re trying to decide if now is the right time to buy a home, let’s connect today to discuss your options.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

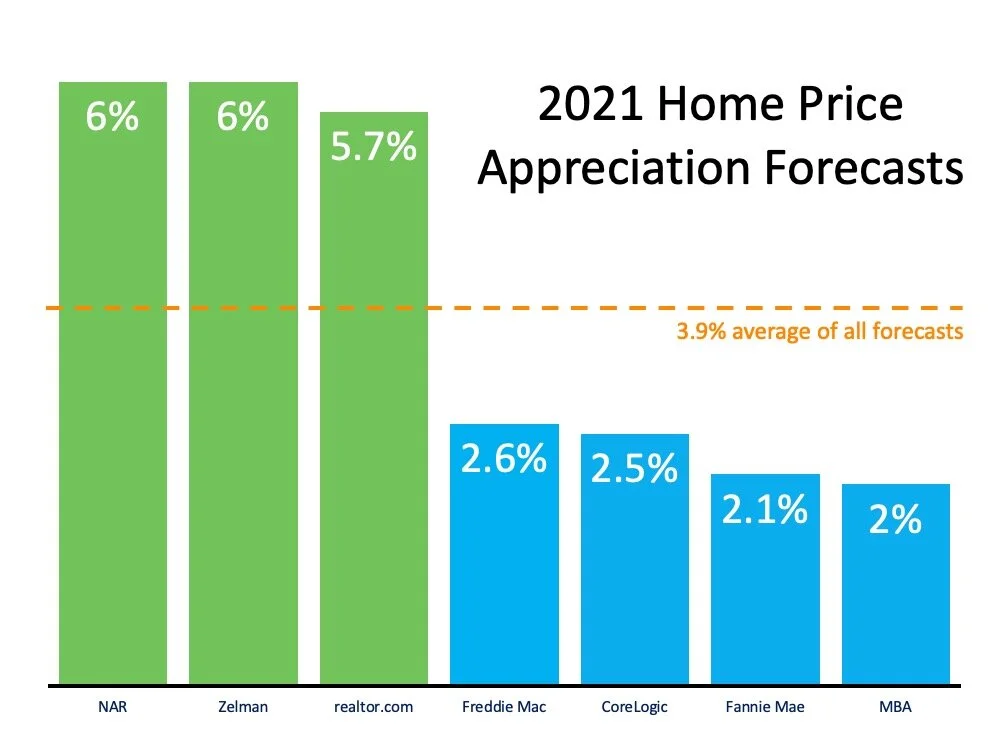

What Does 2021 Have in Store for Home Values?

According to the latest CoreLogic Home Price Insights Report, nationwide home values increased by 8.2% over the last twelve months. The dramatic rise was brought about as the inventory of homes for sale reached historic lows at the same time buyer demand was buoyed by record-low mortgage rates. As CoreLogic explained:

“Home price growth remained consistently elevated throughout 2020. Home sales for the year are expected to register above 2019 levels. Meanwhile, the availability of for-sale homes has dwindled as demand increased and coronavirus (COVID-19) outbreaks continued across the country, which delayed some sellers from putting their homes on the market.

While the pandemic left many in positions of financial insecurity, those who maintained employment and income stability are also incentivized to buy given the record-low mortgage rates available; this is increasing buyer demand while for-sale inventory is in short supply.”

Where will home values go in 2021?

Home price appreciation in 2021 will continue to be determined by this imbalance of supply and demand. If supply remains low and demand is high, prices will continue to increase.

Housing Supply

According to the National Association of Realtors (NAR), the current number of single-family homes for sale is 1,080,000. At the same time last year, that number stood at 1,450,000. We are entering 2021 with approximately 370,000 fewer homes for sale than there were one year ago.

However, there is some speculation that the inventory crush will ease somewhat as we move through the new year for two reasons:

1. As the health crisis eases, more homeowners will be comfortable putting their houses on the market.

2. Some households impacted financially by the pandemic will be forced to sell.

Housing Demand

Low mortgage rates have driven buyer demand over the last twelve months. According to Freddie Mac, rates stood at 3.72% at the beginning of 2020. Today, we’re starting 2021 with rates one full percentage point lower than that. Low rates create a great opportunity for homebuyers, which is one reason why demand is expected to remain high throughout the new year.

Taking into consideration these projections on housing supply and demand, real estate analysts forecast homes will continue to appreciate in 2021, but that appreciation may be at a steadier pace than last year. Here are their forecasts:

Bottom Line

There’s still a very limited number of homes for sale for the great number of purchasers looking to buy them. As a result, the concept of “supply and demand” mandates that home values in the country will continue to appreciate.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Reasons to Hire a Real Estate Professional

Some Highlights

Choosing the right real estate professional to work with is one of the most important decisions you can make in your homebuying or selling process.

The right agent can explain current market conditions and break down exactly what they mean for you.

If you’re considering buying or selling a home this year, let’s connect so you can work with someone who has the experience to answer all of your questions about pricing, contracts, negotiations, and more.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Is This the Year to Sell My House?

If one of the questions you’re asking yourself is, “Should I sell my house this year?” consumer sentiment about selling today should boost your confidence in the right direction. Even with the current health crisis that continues to challenge our nation, Americans still feel good about selling a house. Here’s why.

According to the latest Home Purchase Sentiment Index from Fannie Mae, 57% of consumer respondents to their survey indicate now is a good time to buy a home, while 59% feel it’s a good time to sell one:

“The percentage of respondents who say it is a good time to sell a home remained the same at 59%, while the percentage who say it’s a bad time to sell decreased from 35% to 33%. As a result, the net share of those who say it is a good time to sell increased 2 percentage points month over month.”

As you can see, many still believe that, despite everything going on in the world, it is still a good time to sell a house.

Why is now a good time to sell?

There simply are not enough homes available to meet today’s buyer demand, and they’re selling just as quickly as they’re coming to the market. According to the National Association of Realtors (NAR), unsold inventory available today sits at a 2.3-month supply at the current sales pace, which is down from a 2.5-month supply from the previous month. This record-low inventory is not even half of what we need for a normal or neutral housing market, which should have a 6.0-month supply of unsold inventory to balance out.

With so few homes available for buyers to choose from, we’re in a true sellers’ market. Homeowners ready to make a move right now have the opportunity to negotiate the best possible contracts with buyers who are feeling the pull of intense competition when it comes to finding their dream home. Lawrence Yun, Chief Economist for NAR, notes how quickly homes are selling right now, further confirming the benefits to sellers this season:

“The market is incredibly swift this winter with the listed homes going under contract on average at less than a month due to a backlog of buyers wanting to take advantage of record-low mortgage rates.”

However, this sweet spot for sellers won’t last forever. As more homes are listed this year, this tip toward sellers may start to wane. According to Danielle Hale, Chief Economist at realtor.com, more choices for buyers are on the not-too-distant horizon:

“The bright spot for buyers is that more homes are likely to become available in the last six months of 2021. That should give folks more options to choose from and take away some of their urgency. With a larger selection, buyers may not be forced to make a decision in mere hours and will have more time to make up their minds.”

Bottom Line

If you’re ready to make a move, you can feel good about the current sentiment in the market and the advantageous conditions for today’s sellers. Let’s connect today to determine the best next step when it comes to selling your house this year.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.